The Rise of Embedded Finance: How APIs Are Turning Every App Into a Lender

You know that feeling when you’re shopping online, you hit checkout, and—bam—there’s an option to “Pay in 4” right there? That’s not just a clever button. It’s a tiny glimpse into a massive, quiet revolution. We’re talking about embedded finance. And more specifically, the surge of API-driven lending that’s weaving credit and loans directly into the apps and platforms we already use.

Gone are the days when getting a loan meant visiting a bank branch or even a dedicated finance website. Now, the financial experience comes to you. It happens where you already are: in your accounting software, your e-commerce platform, your business tools. Honestly, it’s like electricity. You don’t think about the power plant; you just plug in and the lamp works. That’s what’s happening with money.

What Exactly Is Embedded Lending? Let’s Break It Down

At its core, embedded lending is the integration of credit products into non-financial customer experiences. It’s not the app being the bank. It’s the app offering the bank’s services, seamlessly, through the magic of APIs—Application Programming Interfaces.

Think of an API as a perfect waiter. Your app (the customer) asks the kitchen (the licensed lender or financial institution) for a specific dish (a loan quote, a credit check). The waiter brings it back exactly as ordered, without the customer ever needing to see the chaos of the kitchen. This API-driven lending model handles the complex, regulated stuff in the background, while the front-end app provides a beautifully simple “Buy Now, Pay Later” or “Get a Business Loan” button.

The Engine Room: Why APIs Changed Everything

This wasn’t really possible a decade ago. Or, well, it was a clunky, expensive nightmare. The rise of cloud computing and open banking regulations cracked the door open. But modern, developer-friendly APIs kicked it right off its hinges.

These APIs allow for:

- Instant Decisions: They can pull and analyze data in milliseconds—transaction history, cash flow, user behavior—to assess risk in real-time.

- Frictionless Onboarding: No more re-typing your business data. With permission, the API pulls it from the platform you’re already using.

- Scalability: A software company can add a lending feature almost as easily as adding a new login button. It’s a product feature, not a new business.

Where You’re Seeing It In Action (Maybe Without Knowing)

This isn’t some futuristic concept. It’s here, solving very real, very specific pain points.

1. The E-Commerce & Retail Checkout

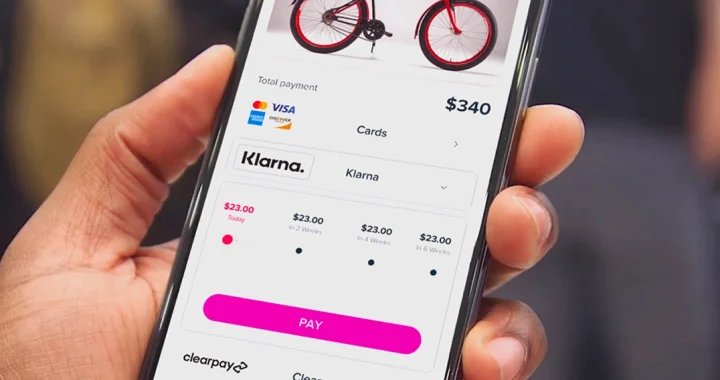

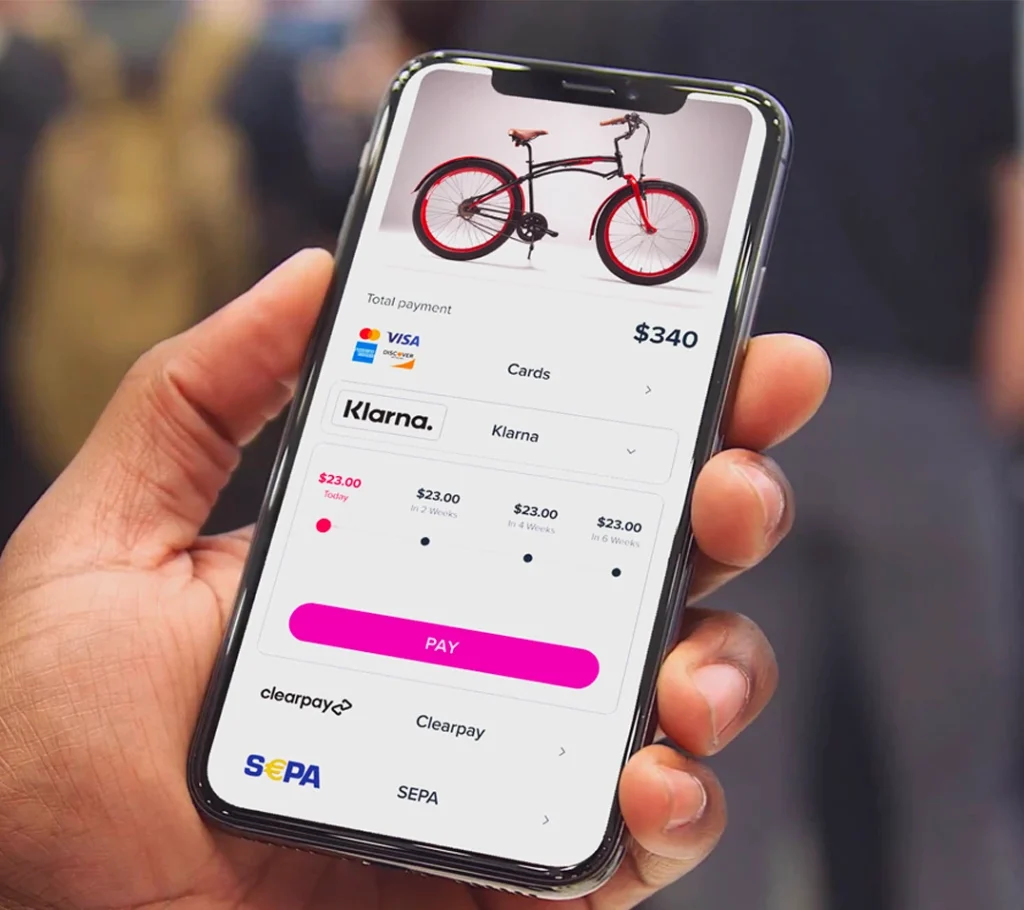

The most obvious one. That “Pay Later” option from providers like Klarna or Affirm? That’s embedded lending. The goal? Reduce cart abandonment by smoothing out the cash flow pinch for the buyer. The merchant gets the full payment upfront, the lender assumes the risk, and the customer gets their stuff. A win-win-win, powered by an API handshake at the moment of truth.

2. Small Business & SaaS Platforms

This is where it gets incredibly powerful. QuickBooks or Xero offering a working capital loan based on your own bookkeeping data. A restaurant management platform providing a line of credit for a new oven during the onboarding flow. An e-commerce platform like Shopify offering loans based on sales history. The platform has the data—the context—which makes the lending decision smarter and more relevant than a traditional bank ever could.

3. Gig Economy & Freelancer Apps

Ride-share or food delivery apps offering cash-outs on earned wages before payday. A freelance marketplace offering a loan to help a designer buy a new laptop for a big project. These are lifelines for a fluid workforce that traditional banks often struggle to serve.

The Good, The Tricky, and The Future

Like any seismic shift, this brings huge opportunities and… well, a few headaches to figure out.

The Upside is Massive: For consumers and businesses, it means access. Financial products are more contextual, convenient, and often more inclusive. For the apps and platforms (the “embedders”), it’s a golden ticket. They deepen user engagement, unlock new revenue streams, and create a stickier, more valuable product without becoming a bank themselves.

The Challenges are Real: With great power comes great regulatory scrutiny. Compliance (like KYC and AML) is non-negotiable and complex. Who owns the customer experience when something goes wrong—the app or the lender? And there’s a delicate balance to strike: making lending accessible shouldn’t mean encouraging irresponsible debt. Transparency is absolutely key.

Let’s look at the dynamics in a simple table:

| Stakeholder | Biggest Win | Key Concern |

| End-User (Borrower) | Unbelievable convenience & contextual offers | Data privacy, understanding loan terms |

| Platform/App (Embedder) | Increased revenue & user retention | Managing regulatory risk & brand reputation |

| Lender/Bank (Provider) | New, efficient customer acquisition channel | Maintaining underwriting control & compliance |

So, What’s Next? The Lines Keep Blurring

We’re only in the second inning of this game. The future of embedded and API-driven lending isn’t just about a loan at checkout. It’s about hyper-contextual financial products. Imagine:

- A property management software offering a lease-deposit loan the second a tenant is approved.

- An electric vehicle charging app financing the home charger installation right in its flow.

- Healthcare portals offering tailored payment plans for procedures, backed by real-time insurance data.

The technology will get smarter. AI and more holistic data sharing (with user consent, of course) will lead to even more accurate, fair risk models. And honestly, the very definition of a “financial service” will keep stretching.

The bottom line? Finance is ceasing to be a destination. It’s becoming a feature. A utility. It’s woven into the fabric of our digital lives so tightly that we’ll soon stop remarking on its “embedded” nature—it’ll just be how things work. The companies that understand this shift, that prioritize seamless, ethical, and helpful integrations, won’t just be building better apps. They’ll be building the financial ecosystem of tomorrow, one API call at a time.